You may have heard your accountant or bank manager talk about your “balance sheet” and “profit and loss account”. What do these terms mean, and what information can these documents provide you about your company?

The balance sheet and profit and loss account tell you different things. The balance sheet shows what your company owns and owes at a particular point in time, while the profit and loss account shows how much income and profit the business has generated over a period such as a month, quarter or year.

Emily Coltman FCA, Chief Accountant to FreeAgent – who provides the UK’s market-leading online accounting system specifically designed for small businesses and freelancers – explains.

Balance sheet

The balance sheet gives you a snapshot of how much your business owns (its assets) and how much it owes (its liabilities) at a given point in time. That might be today, or it might be at the end of your business’s accounting year.

The top half of the balance sheet starts with the business’s assets. These are divided into fixed assets, such as large items of equipment such as computers and furniture, and current assets.

Current assets are more easily and quickly converted into cold hard cash, like money owed by customers and in the bank.

The balance sheet then shows the business’s liabilities, which are divided into current liabilities, money due within a year, like tax bills, and money owed to staff. Long-term liabilities are those due in more than a year, like a mortgage or a bank loan.

There will then be a total of all the business’s assets minus its liabilities.

If the business were to sell all its assets off and pay all its debts, anything left over would be available for its owner(s) to draw out.

That’s why the bottom half of the balance sheet is headed up something like “Owners’ Equity”, “Owners’ Capital”, or “Shareholders’ Funds”.

The total of the bottom half of the balance sheet will equal the top half. These two totals are called the balance sheet total.

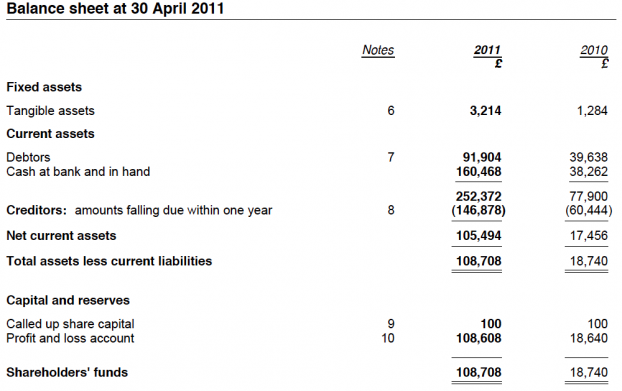

Here is an example of a typical balance sheet for a small limited company:

If your business owns more than it owes, the balance sheet total will be positive. If your business owes more than it owns, the balance sheet total will be negative. This is not good news because it means your business lacks enough money to pay all its debts.

In addition to this quick check, you can use your balance sheet to calculate useful ratios.

For example, if you divide the current assets figure by the current liabilities, you’ll see if your business has enough money to meet all its immediate obligations.

If this figure is less than 1, alarm bells should start ringing.

If your business sells goods, try working this ratio out, starting with the current assets excluding stock.

This will show you whether your business’s stock couldn’t be sold. For example, if it were destroyed in a fire or flood, or went off, or went out of fashion – your business would still have enough money easily available to pay its imminent debts.

Profit and loss account

This is often called the P&L for short, and it shows your business’s income, less its day-to-day running costs, over a given period of time – often a year, month, or quarter.

The day-to-day running costs divide up into direct costs, which are costs that relate immediately to sales, and overheads, which are general running costs.

For example, the cost of buying materials to make goods to sell, and the cost of delivering finished goods to customers, would be direct costs.

Renting an office would be an overhead. If your business sells services, it may not have any direct costs.

Your business’s income from sales is called turnover.

Turnover minus direct costs gives a figure called gross profit. A business’s total income, less all its day-to-day running costs, is its net profit.

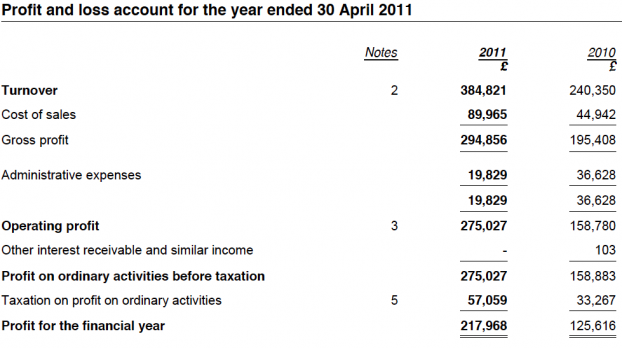

Here is an example of a typical P&L account for a small limited company:

You can work out your business’s gross profit margin by dividing the gross profit by turnover, and the net profit margin by dividing its net profit by its turnover. This shows you how much profit your business makes for every pound of sales.

These calculations are most valuable when you compare the margin for one period to another.

For example, if your margin has gone up from one year to the next, that means you’re keeping more of your income from sales than before, perhaps because you’ve raised your prices or are saving money on a cost.

If, on the other hand, your margin fell from one year to the next, you’re not keeping as much of your income from sales as before, and you may need to take action to remedy that.

For more information, to grow your business using the profit margin calculations.

As you can see, the balance sheet and P&L aren’t just for your accountant!

You can use them to collate a lot of useful information about your business’s financial health and to help you make essential business decisions.

Further Information

Emily Coltman FCA is Chief Accountant to FreeAgent, who provides the UK’s market-leading online accounting system specifically designed for micro-businesses and freelancers.

Try it for free at www.freeagent.com.

Top contractor accountants

- SG Accounting – First 3 months half price (£59.50 per month)

- Bright Ideas Accountancy – 5 stars on Google, from £109 per month

- Clever Accounts – IR35 FLEX. Take on any contract type

- Aardvark Accounting – Complete service from £89 per month

- Integro Accounting – Fixed fee – 6 months half price

We've worked with all of these firms for over 8 years. Always check current pricing and service details before signing up.